A number stories in European financial markets last week are connected by increasing concerns within the investment community about what Europe’s future has in store. Swiss central bankers abandoned their currency peg, Greek commercial bankers asked for emergency liquidity assistance, and German economists raised questions about the deterioration of Italy’s position within the Target2 system.

Worse, each of these developments feeds into new uncertainties — about whether other countries will follow Switzerland’s example or take preventative measures to lower the market pressure on their national currencies, about whether Greek banks will experience an accelerating run on their deposits now that their liquidity has been questioned, about whether the German government and the Bundesbank will increase the pressure for restraints on any ECB program for quantitative easing, and about whether the Italian presidential elections will further undermine international confidence in the Italy’s banks.

My point is not that these things are all going to come to pass. These are possibilities. As such, they give investors a good reason to move their capital from high-risk to low-risk investments, to bring it closer to home, and to make it easier to convert into cash (or more liquid). Moreover, this isn’t a new phenomenon. It is an ongoing mechanism. And it is the ongoing nature of the mechanism that is important because the flows of capital deplete stocks (or buffers) in some places, making them more vulnerable to sudden shocks, while building up stocks in other places where they threaten to create another round of distortions.

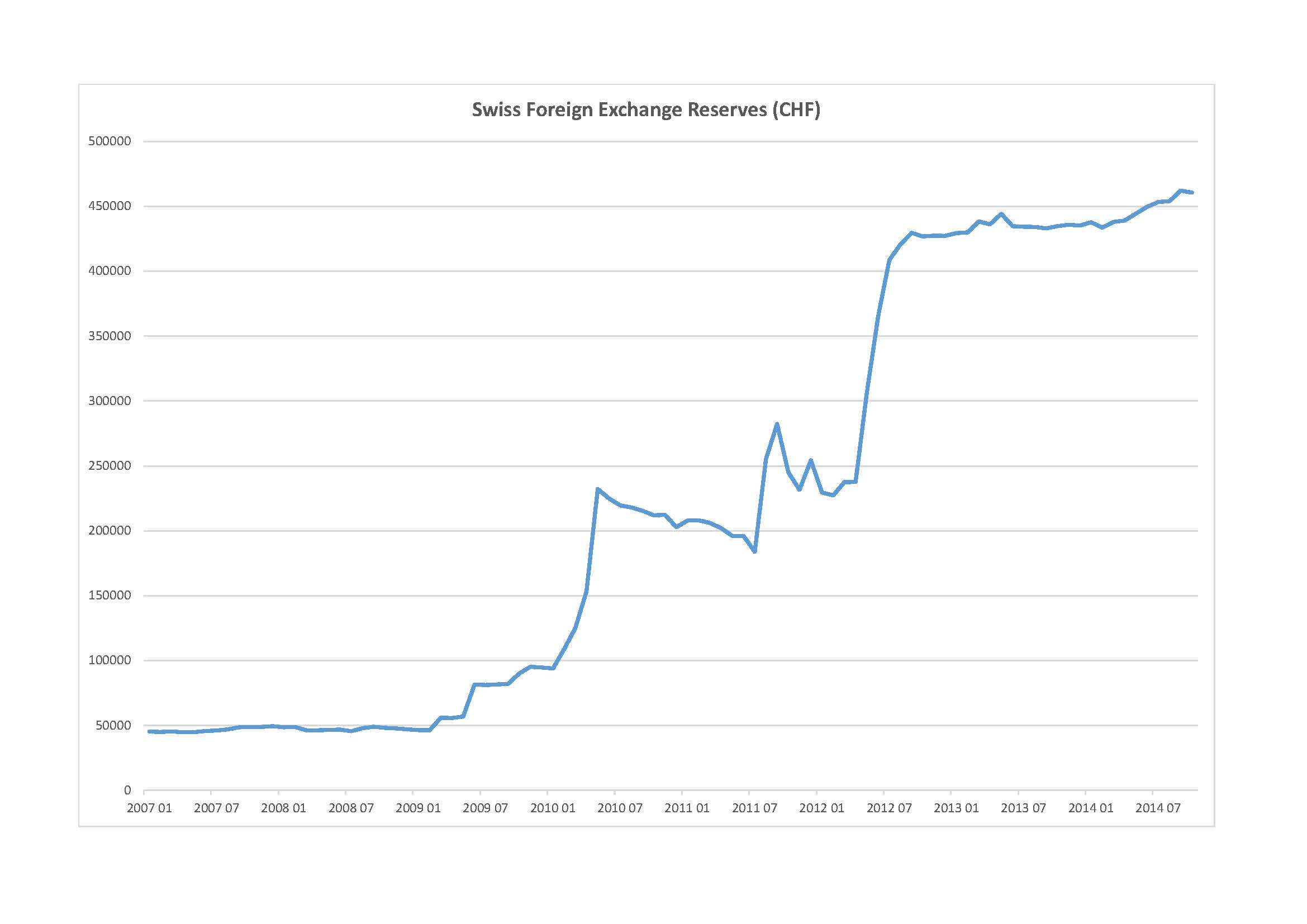

Consider the Swiss case. Switzerland is a safe haven where people put their money in times of duress. Hence if you look at the evolution of Swiss foreign exchange reserves, you will see big jumps during the period surrounding the Greek bailout in the spring of 2010 and during the onset of the Italian sovereign debt crisis in the summer of 2011. That second jump is what inspired the Swiss central bank to peg the value of the Swiss Franc to the euro in the hopes of reducing the incentives for speculators to look for profits in an appreciating exchange rate.

The Swiss currency peg had little impact on investors who seek to preserve their capital and so there is another massive jump in the volume of Swiss foreign exchange reserves in the spring and summer of 2012. The further accumulation of reserves only stopped once European Central Bank (ECB) President Mario Draghi promised to do ‘whatever it takes’ to safeguard the euro. From September 2012 onward, the volume of Swiss foreign exchange reserves increased only very gradually by comparison. Nevertheless, the Swiss central bank worried that the divergence between the world’s main central banks – meaning essentially the ECB and the United States Federal Reserve – would spark another surge of capital into the country. According to its official press release, the Swiss central bank remains committed to intervene in for exchange markets but it does not want to have to defend the value of the currency. The question is whether that distinction will actually save it from accumulating more foreign exchange reserves – even when measured in an appreciating Swiss franc.

The Greek case is connected both to the general uncertainty and to the Swiss case. Investors have been pulling their money out of Greek banks and putting it elsewhere in the euro area in response to increasing speculation that a new Greek government could leave the single currency, even if only by accident, and that other euro area countries will not stand in the way. Such concerns are overblown – as European central bankers like Benoît Cœuré have insisted repeatedly – but that fact does not make it any less rational for Greek savers to hedge their bets. Meanwhile, Reuters reports that executives at Alpha Bank and Eurobank in Greece are looking at emergency liquidity assistance as a precaution in light of their exposure to mortgages in Swiss francs. Such exposure is not limited to Greece. Some, like Hungary, have managed to reduce their vulnerability to sudden changes in the exchange rate; others, like Poland, are less fortunate.

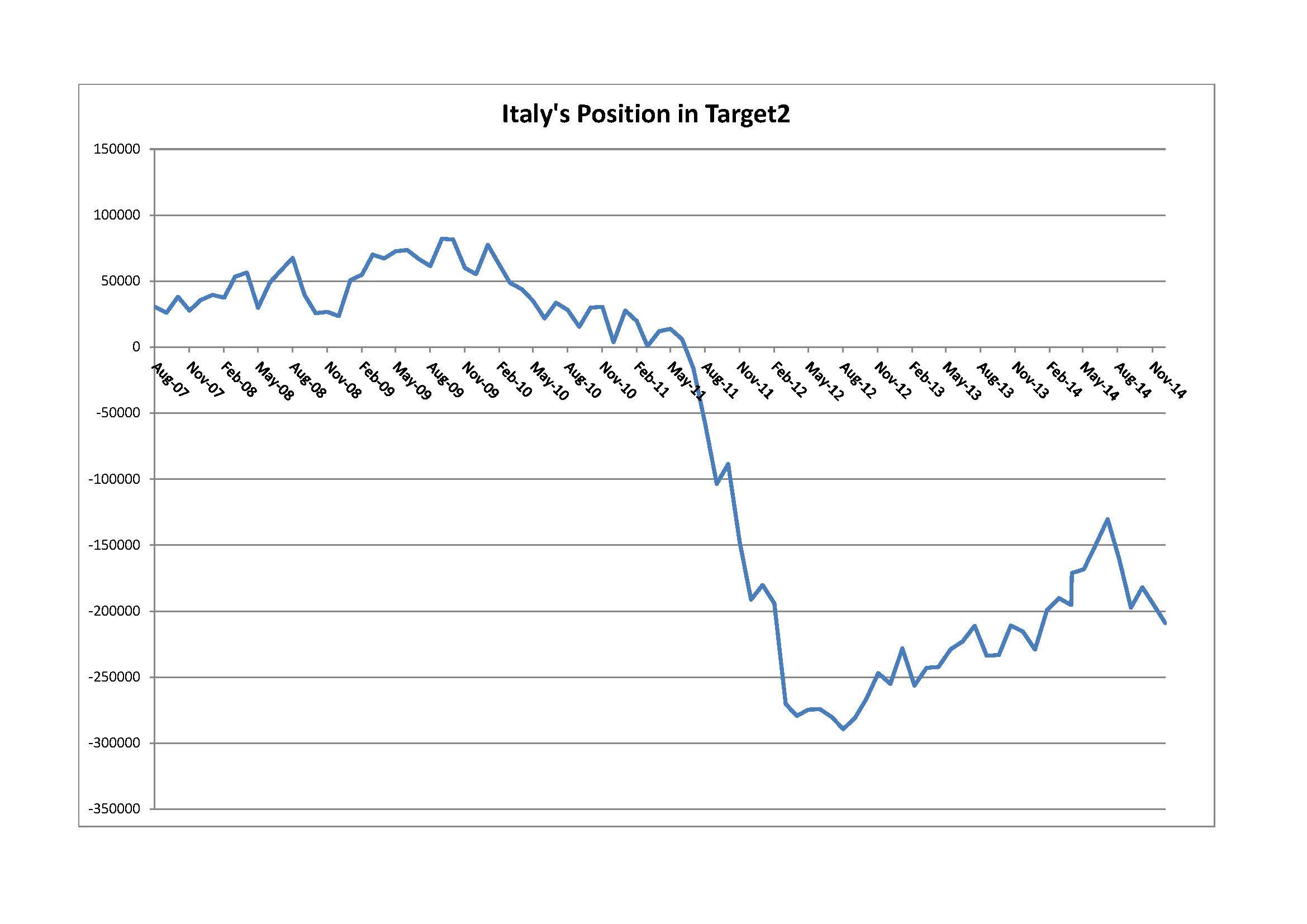

Then there is the situation in Italy. What a country’s Target2 position reveals is the extent to which it has a gap in its balance of payments between current transactions related to the flow of goods and services and capital transactions related to the movement of money and investments. Historically, Italy has been a net creditor for the euro system as a whole, which means that at some point it attracted more money or investment than was necessary to finance the trade in goods and services. That all began to change during the run-up to the Greek bailout and Italy’s Target2 position began to deteriorate (much as Switzerland’s foreign exchange reserves began to accumulate). The last month that Italy showed a positive balance on its Target2 position was June 2011. After that, money flowed out of Italy faster than Italy’s trade in goods and services could adapt. The change in Italy’s Target2 position is the gap in its balance of payments. What is interesting to note in the data is just how quickly that gap opened up. By its peak in August 2012, Italy had a negative balance of just under €290 billion.

Again, we can see the impact of Draghi’s ‘whatever it takes’ commitment. From August 2012 to July 2014, capital flows back into Italy above and beyond its requirements to finance the trade in goods and services. Even though the country’s position on Target2 is negative, it is decreasing – which is a positive gap in the balance of payments. There is some volatility in the numbers, due in part to the ‘end-of-month’ reporting in this data series as the Bank of Italy has noted, but the trend is clear. The question is why it reverses again in July 2014. Part of the answer – as explained by the Bank of Italy to Wolfgang Munchau’s team at Eurointelligence – is that the Italian government was able to redeem some of its debt without rolling it over, and hence any international investors whose positions matured were left with cash to redeploy elsewhere. But part of the answer is that people holding deposits in Italian banks were moving their money out of Italy. Some of this may have gone into Switzerland, but that is just speculation. The only important point is that it left the country. Moreover, Italy’s experience is relatively unique in this respect. By contrast, the situation in Spain appears more stable.

If we add this all up, it suggests that important parts of the European financial economy remain vulnerable to the forces of disintegration. Despite the progress made in creating a banking union and the prospect of a capital union on top of it, investors remain unconvinced by the promise of the single market. This is not a good sign. The European Central Bank warned last April that Europe had made insufficient progress in re-integrating financial markets since the crisis. They still have a long way to go.

Follow @Erik_Jones_SAIS

[…] “important parts of the European financial economy remain vulnerable to the forces of disintegration. Despite the progress made in creating a banking union and the prospect of a capital union on top of it, investors remain unconvinced by the promise of the single market. This is not a good sign. The European Central Bank warned last April that Europe had made insufficient progress in re-integrating financial markets since the crisis. They still have a long way to go.” (18 January – The Threat of Financial Disintegration) […]

LikeLike